Endesa Chile IR presentationAs of December 2012

Endesa Chile IR presentation YE 2012

2

Multinational electricity generation company based in Chile.

Efficient and diversified investment portfolio of generation assets.

Part of an important worldwide electricity group (Enel, Endesa, Enersis).

Our company

Vast experience, with over 69 years of history.

Conservative commercial policy leading to revenue and margin stability.

Among the most actively traded companies in Chilean stock markets.

Endesa Chile IR presentation YE 2012

3

•COSTANERA, 70%

•EL CHOCÓN, 65%•EDEGEL, 62%•EMGESA, 27%

•ENDESA BRASIL, 39%

AMPLA

COELCE

FORTALEZA

CDSA

CIEN

61%

92%

60%

PEHUENCHE, 93%

CELTA, 100%

SAN ISIDRO, 96%

ENDESA ECO, 100%

CANELA, 75%

Ownership Structure

60%14%

6%

5%4%

11%

ENERSIS

Chilean Pension Funds

Institutional Shareholders

ADR Holders

Minority Shareholders

Other Institutional Shareholders

Endesa Chile IR presentation YE 2012

4

A unique portfolio in LATAM’s Generation business

COLOMBIA

2,914 MW inst. capacity

Hydro: 2,470 MW

Thermal : 444 MW

20% market share

No. 2

5,961 MW inst. capacity

Hydro: 3.456 MW

Thermal : 2,418 MW

NCRE: 87 MW

33% market share

PERU

1,657 MW inst. capacity

Hydro: 746 MW

Thermal : 911 MW

24% market share

CHILE

BRAZIL

987 MW inst. capacity

Hydro: 665 MW

Thermal : 322 MW

1% market share in

generation

Consolidated installed capacity: 14,185 MW

Capacity including Brazil: 15,172 MW

Consolidated energy sales 2012: 59,020 GWh

3,652 MW inst. capacity

Hydro: 1,328 MW

Thermal: 2.324 MW

12% market share

ARGENTINA

No. 1

No. 1

No. 1

Endesa Chile IR presentation YE 2012

5

Results affected by the drought in Chile and high fuel costs

1Amounts expressed in US$, using the average exchange rate for the period (Ch$486.59 per US$).2 Net of “Foreign currency exchange differences”.

3 Closing share price for each year.

Indicator2011

MM ch$

2012

MM ch$Change

2012

MM US$1

Revenues 2,404,490 2,369,386 (1%)4,869

Operational Expenses (1,217,260) (1,328,703) 9%(2,731)

Contribution margin 1,187,230 1,040,684 (12%)2,139

EBITDA 973,890 833,850 (14%)1,714

EBIT 787,971 632,209 (20%)1,299

Net finance expenses2

(114,829) (135,294)18%

(278)

Net income before

taxes 791,719 604,513 (24%)

1,242

Net income 581,155 419,043 (28%)861

Net attributable income 446,874 234,335 (48%)482

EBITDA Margin 40.5% 35.2% (13%) -

Profit Margin 24.2% 17.7% (27%) -

E.P.S. 54.5 28.6 (51%) 2

P/E3 14.1 27.2 106% -

Endesa Chile IR presentation YE 2012

Chile42%

Colombia20%

Peru12%

Argentina26%

Chile38%

Colombia25%

Peru16%

Argentina21%

Chile35%

Colombia45%

Peru17%

Argentina3%

6

EBITDA by Country

Total Installed Capacity: 14,185 MW

EBITDA 2012:

US$ 1,714 million

Total Generation : 53,517 GWh

Endesa Brasil

• Endesa Chile’s ownership: 40% (38.9%direct).

• Net Attributable Income1: US$ 221 million.

1 Considers the total contributions of Endesa Brasil recognized by Endesa Chile as an equity method investment.

Endesa Chile IR presentation YE 2012

66%

30%

4%

53%

19%

28%

65%

30%

5%

18%

82%

61%

31%

8%

51%

19%

30%

64%27%

9% 19%

81%

7

Prudent Commercial Policy

Regulated SpotFree Clients

Physical Sales as 2011

Chile Colombia Peru

Regulated SpotFree Clients

Argentina

Physical Sales as 2012

Chile Colombia Peru Argentina

Endesa Chile IR presentation YE 2012

8

Debt by Type Debt by CurrencyDebt by Country

Amounts expressed in US$, using the close exchange rate for the period (Ch$ 479.96 per US$)1 For year 2012 considers “Cash and cash equivalents” and “Other current financial assets”.

Strong Financial Position

Chile, 49%

Argentina, 7%

Colombia, 36%

Peru, 8%

Local Currency,

41%

US$, 49%

UF, 10%Others,

13%

Bank Debt, 15%

Bonds, 72%

Indicator2011

MM Ch$

2012

MM Ch$Change % Change

2012

MM US$

Gross Debt 1,808,969 1,958,068(149,098)

(8%)4,080

Cash1 421,282 301,914119,368

40%630

Net Debt 1,387,687 1,656,153(268,466)

(16%)3,450

Leverage 0.91 0.89(0.01)

(1%)0.89

Financial Expenses

Coverage6.52 5.18

(1.63)(31%)

5.18

Endesa Chile IR presentation YE 2012

9

1 Payments for additions of fixed assets.2 For year 2012 considers only the interim dividend paid on January 24th, 2013.

Amounts are expressed in US$, using the average exchange rate for each period.

Free Cash Flow (US$ million)

2.248

(305)

(564)

(308)

1.070

(394)

2.098

(235)

(499)(353)

1.012

(523)

2.014

(251)

(551)(435)

776

(462)

1.714

(300)

(538)(381)

494

(51)

EBITDA Net Financial Result CAPEX Income Tax FCF Dividends

2009 2010 2011 2012

Endesa Chile IR presentation YE 2012

10

Electricity demand Evolution in LATAM

4.4%

2.2%

5.3%

5.5%

3.3%

80%

90%

100%

110%

120%

130%

140%

150%

160%

170%

180%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

To

tal

Sale

s i

n G

Wh

(%

gro

wth

)

Historic electricity demand growth (CAGR, last ten years)

CHILE COLOMBIA PERU ARGENTINA BRAZIL

Endesa Chile IR presentation YE 2012

11

Direct relation between GDP and electricity demand

ARGENTINA

AUSTRALIA

AUSTRIA

BOLIVIA

BRAZIL

CANADA

CHILE

COLOMBIA

FRANCE

GERMANY

INDIA

ITALY

JAPAN

MEXICO

PERU

SPAIN

UNITED KINGDOM

UNITED STATES

CHINA

RUSSIA

FINLAND

GREECE

IRELAND

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

0 5000 10000 15000 20000 25000 30000 35000 40000 45000

Ele

ctr

icit

y c

on

su

mp

tio

n,

per

cap

ita (

Kw

h p

er

year)

Income per capita (Fixed PPP $)

Data source: International Energy Agency (EIA) and The World Bank.

Chile aims to be in the group of developed countries.

There is no development without energy.

Endesa Chile IR presentation YE 2012

12

Expected Evolution for Endesa Chile Installed Capacity

13,845 13.845 13.845 13.845

350 350 350

400 400

145 145 88

150

188

740

490

2011 2012 Under Construction On Basic Engineering

Percentage increase over installed capacity, year 2011 (13.845 MW)

Year 2011 Bocamina II Quimbo Salaco Renaico Los Condores Curibamba Punta Alcalde Neltume

3%

6%

18%

Endesa Chile IR presentation YE 2012

13

Bocamina II

• Thermal, coal fired power plant

• Located in Coronel, Bío-Bío region

• 350 MW of installed capacity

• Estimated load factor: 65%

• Capex: US$ 841 MM Investment

• On October 29th, 2012, Bocamina II started its

commercial operations with the formal approval

from the authority.

• Approx 510 GWh1 generated during year 2012.

New Plant Start-Up Increasing Capacity

1IEstimated generation including tests.

Endesa Chile IR presentation YE 2012

El Quimbo

• Hydro power plant.

• Located in Huila Department

• Utilizes stream coming from Magdalena river

• 400 MW of installed capacity

• Estimated load factor: 60%

• River detour in March 2012

• Capex: US$ 837 MM investment

• Estimated start-up: December 2014

14

Projects Under Construction

Endesa Chile IR presentation YE 2012

15

Projects Under Construction

Salaco Chain (optimization)

• Repowering the minor plants to reach a

260 MW power.

• Located in the Bogota River system.

• Optimization works started on January

2013.

• 145 MW will be added to the current

capacity (482 GWh/year).

• Estimated start-up: 4th quarter 2013 (first

unit).

Endesa Chile IR presentation YE 2012

16

Projects Under Study

Los Cóndores

• Hydro power plant

• Located in San Clemente, in Maule

region

• 150 MW of installed capacity

• Estimated load factor: 46%

• EIS approved.

Punta Alcalde

• Thermal, coal-steam power plant

• Located in Huasco, in Atacama region

(SIC)

• 740 MW of installed capacity

• Estimated load factor: 83%

• EIS approved by the Ministers

Committee on Dec 03th 2012

Endesa Chile IR presentation YE 2012

17

Projects Under Study

Curibamba

• Hydro power plant

• Located in Junín department,

utilizes streams coming from

Comas and Uchubamba rivers

• 188 MW of installed capacity

• Estimated load factor: 61%

• EIS approved.

Renaico

• Wind farm

• Located in Araucanía region (SIC)

• 88 MW of installed capacity

• EID approved for the generation

plants.

Endesa Chile IR presentation YE 2012

18

Projects Under Study

Neltume

• Hydro power plant, run of the river

• Located in Panguipulli, in Los Ríos

region (SIC).

• 490 MW of installed capacity.

Endesa Chile IR presentation YE 2012

19

Projects Under Study

Hidroaysén

• Hydro power plant located in Aysén region

• 2,750 MW of installed capacity

• EIS approved for the generation plants (5)

• One of the most efficient hydroelectric projects in

the world, using renewable resources

• Average load factor: 77%

• Endesa Chile owns 51% and Colbún 49%.

• CO2 emissions: Reduction of 16.2 million tons/year

312

144 134

81 81 75 69 65 54 54 53 45 4129 23 12 12 7

0

50

100

150

200

250

300

350

GW

h /

ye

ar-k

m2

Energy / Flooded Surface

Endesa Chile IR presentation YE 2012

10,072 10,393 9,428

13,963 15,364

12,102 13,297

2006 2007 2008 2009 2010 2011 2012

1 Amounts expressed in US$, using the average exchange rate for each period.2 Amounts expressed in US$, using the last exchange rate for each period.3 Considers only the interim dividend paid in January 24, 2013 20

Dividends

(Ch$ per Share)EBITDA

(US$ Million)

Market Value

(US$ Million)

Market Value and Dividends

1

Source: Intern using Bloomberg

2

1.503 1.671

2.033 2.248

2.098 2.014

1.714

2006 2007 2008 2009 2010 2011 2012

13.8

21.3

26.8

32.5

27.2

3,04

2007 2008 2009 2010 2011 2012

3.02

3

Endesa Chile IR presentation YE 2012

21

Contact us at:

Juan Pablo Vicuña

Investor Relations Executive

(56-2) 2630 9585

Susana Rey

Investor Relations Director

(56-2) 2630 9606

Catalina Gonzalez

Head of Investor Relations

(56-2) 2630 9603

Guillermo Berguecio

Investor Relations Executive

(56-2) 2630 9506

Endesa Chile’s Investor Relations Team

Endesa Chile IR presentation YE 2012

22

EXHIBITS

Endesa Chile IR presentation YE 2012

23

Lower hydro generation in Chile, mainly explained by a third consecutive year of a severe drought.

Highlights of 2012

29% increase in Colombian EBITDA, mainly related to higher hydro generation and spot prices.

Non-recurring accounting effects in Colombia and Peru.

6% growth of installed capacity in Chile, related to Bocamina II start up.

14% decrease in consolidated EBITDA explained by our operations in Chile, Argentina and Peru.

Indemnity insurance related to Bocamina II.

Endesa Chile IR presentation YE 2012

24

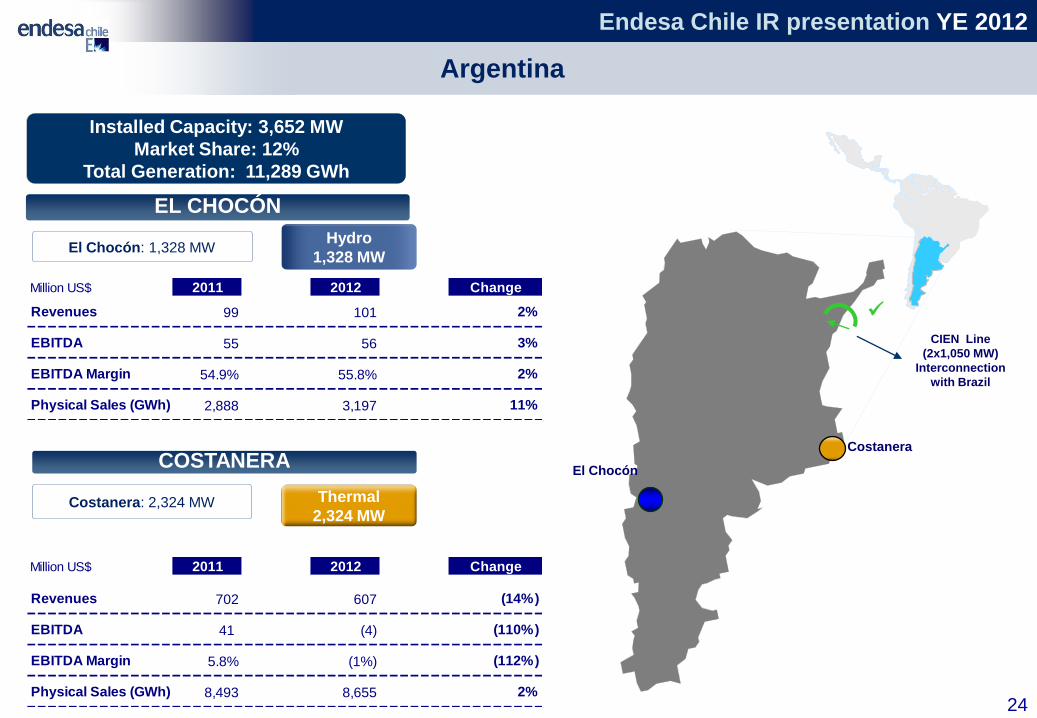

Argentina

Costanera: 2,324 MW

El Chocón: 1,328 MWHydro

1,328 MW

Installed Capacity: 3,652 MW

Market Share: 12%

Total Generation: 11,289 GWh

EL CHOCÓN

COSTANERA

Thermal

2,324 MW

El Chocón

Costanera

CIEN Line

(2x1,050 MW)

Interconnection

with Brazil

Million US$ 2011 2012 Change

Revenues 99 101 2%

EBITDA 55 56 3%

EBITDA Margin 54.9% 55.8% 2%

Physical Sales (GWh) 2,888 3,197 11%

Million US$ 2011 2012 Change

Revenues 702 607 (14%)

EBITDA 41 (4) (110%)

EBITDA Margin 5.8% (1%) (112%)

Physical Sales (GWh) 8,493 8,655 2%

Endesa Chile IR presentation YE 2012

25

Lima:

• Edegel (Gx)

Ventanilla: 485 MW

Santa Rosa: 426 MW

55% Thermal

911 MW

Cuenca Río Rímac: 552 MW

Yanango: 43 MW

Chimay: 151 MW

45% Hydro

746 MW

Installed Capacity: 1,657 MW

Market Share: 23%

Total Generation: 8,740 GWh

EDEGEL

Peru

Million US$ 2011 2012 Change

Revenues 493 580 18%

EBITDA 290 287 (1%)

EBITDA Margin 58.9% 49.6% (16%)

Physical Sales (GWh) 9,450 9,587 1%

Endesa Chile IR presentation YE 2012

26

Installed Capacity1: 5,961 MW

Market Share: 33%

Total Generation: 20,194 GWh

ENDESA CHILE

D. Almagro–Taltal

Bocamina Laja

Maule

Bio Bio

Tarapaca

Huasco

San Isidro

Los Molles

Cachapoal

Santiago

Los Molles: 18 MW

Rapel-Sauzal: 466 MW

Maule: 875 MW

Laja: 940 MW

Ralco-Pangue: 1,157 MW

58% Hydro

3,456 MW

41% Thermal

2,418 MW

Tarapaca-G.Atacama: 572 MW

D. Almagro–Taltal: 269 MW

Huasco: 64 MW

San Isidro 1 and 2: 778 MW

Bocamina: 128 MW

Bocamina II: 350 MW

TG Quintero: 257 MW

1% NCRE

87 MW

Canela: 18 MW

Canela II: 60 MW

Ojos de Agua: 9MW

Chile

Million US$ 2011 2012 Change

Revenues 2,624 2,391 (9%)

EBITDA 1,019 602 (41%)

EBITDA Margin 38.8% 25.2% (35%)

Physical Sales (GWh) 22,070 21,277 (4%)

Endesa Chile IR presentation YE 2012

27

Guavio: 1,213 MW

Betania: 541 MW

Río Bogotá: 716 MW

85% Hydro

2,470 MW

15% Thermal

444 MW

Cartagena: 208 MW

Termozipa: 236 MW

Installed Capacity: 2,914 MW

Market Share: 20%

Total Generation: 13,294 GWh

EMGESA

Cartagena

Bogotá

Colombia

Million US$ 2011 2012 Change

Revenues 1,025 1,192 16%

EBITDA 598 773 29%

EBITDA Margin 58.3% 64.8% 11%

Physical Sales (GWh) 15,112 16,304 8%

Endesa Chile IR presentation YE 2012

28

Fortaleza: 322 MWThermal

322 MW

Cachoeira: 665 MW Hydro

665 MW

Installed Capacity: 987 MW

Market Share: 1%

Total Generation: 5,177 GWh

CACHOEIRA

FORTALEZA

Fortaleza

Rio de Janeiro

Two 500 Km lines

Total interconnection capacity: 2,100 MW

CIEN1: Transmission

Brazil-Argentina Interconnection

Brazil

Cachoeira

1Includes CIEN, CTM and TESA

Million US$ 2011 2012 Change

Revenues 260 319 23%

EBITDA 193 229 19%

EBITDA Margin 74.0% 71.9% (3%)

Physical Sales (GWh) 3,986 4,344 9%

Million US$ 2011 2012 Change

Revenues 266 286 7%

EBITDA 118 99 (16%)

EBITDA Margin 44.3% 34.8% (21%)

Physical Sales (GWh) 2,842 2,947 4%

Million US$ 2011 2012 Change

Revenues 123 149 21%

EBITDA 174 105 (40%)

EBITDA Margin 141.6% 70.3% (50%)

Endesa Chile IR presentation YE 2012

29

Installed Capacity, and Energy Generation

Installed

Capacity

Generation

MW 12M 2012

Chile Colombia Brazil Peru Argentina Total

Total 5,961 2,914 986.7 1,657 3,652 15,172

Hydro 3,456 2,471 665 746 1,328 8,666

Nuclear - - - - - -

Coal 636 236 - - - 872

Oil-Gas 1,782 208 322 911 2,324 5,547

CHP / Renewables 87 - - - - 87

MWh 12M 2012

chg. Vs. 12M 2011

Chile Colombia Brazil Peru Argentina Total

Total 20,194 -2.5% 13,294 10.0% 5,177 24.6% 8,740 -4.5% 11,289 4.5% 58,694 3.1%

Hydro 11,171 -5.9% 12,692 9.2% 3,722 19.3% 4,599 -0.3% 2,801 16.5% 34,985 4.0%

Nuclear 0 - 0 - 0 - 0 - 0 - 0 -

Coal 2,337 28.4% 398 51.0% 0 - 0 - 0 - 2,735 31.3%

Oil-Gas 6,483 -5.4% 203 -1.5% 1,454 40.7% 4,141 -8.7% 8,488 1.1% 20,770 -1.2%

CHP / Renewables 204 17.6% 0 - 0 - 0 - 0 - 204 17.6%

Endesa Chile IR presentation YE 2012

30

Feb. 2010Jan. 2010 Apr. 2011

BBB+ Baa2 BBB+

Since:

Affirmed: Dec. 2012 Oct. 2012

Credit Risk Ratings

Jun. 2012

Financial Debt

Healthy Debt Profile and Credit Risk Ratings

US$ Millions 2013 2014 2015 2016 2017 Balance TOTAL

Chile668 140 220 16 13 928 1,985

Argentina230 36 7

- - -273

Perú54 54 36 60 50 83 336

Colombia -80 164 23

119 1,099 1,486

TOTAL952 310 428 99 181 2,110 4,080

Endesa Chile IR presentation YE 2012

31

Net debt/EBITDA EBITDA/Net financial expenses

1 EBITDA / (Financial expenses + Income (Loss) for indexed assets and liabilities + Foreign currency exchange differences, net)

Endesa Chile 2011 2012

Financial Expense Coverage1 6.5 5.2

ROE (%) 18.1% 9.2%

ROA (%) 9.2% 6.4%

Principal Financial Ratios

5.6

7.4

8.9

8.0

5.7

2008 2009 2010 2011 2012

2.0

1.5 1.5 1.5

2.0

2008 2009 2010 2011 2012

Endesa Chile IR presentation YE 2012

32

American Stock Market Spanish Stock Market

NYSE (US$)1

Price 2012 (Avg) 49.1Max 2012 55.4

Min 2012 40.6Daily Avg Trans Vol (million

ADR) 0.13Avg Daily Trans (US$ million

traded) 6.42

LATIBEX (€)

Price 2012 TTM (Avg) 1.3Max 2012 TTM 1.5

Min 2012 TTM 1.0Daily Avg Trans Vol (million

shares) 0.01Avg Daily Trans (€ million

traded) 0.02

Chilean Stock Market

BOLSA DE SANTIAGO (CLP)

Price 2012 (Avg) 808.5Max 2012 894.0

Min 2012 700.5Daily Avg Trans Vol (million

shares) 5.18Avg Daily Trans (CLP million

traded) 4,172.8

Relevant Stock Presence

1 Considers NYSE and others stock markets within the USA.2 Includes “Bolsa de Valparaiso” and “Bolsa electrónica de Chile”

Source: Intern, using Bloomberg

Average Daily Trans (US$ MM)

$ 9.03; 58%

$ 6.48; 42%

$ 0.02; <1%

Santiago Stock Exchange NYSE LATIBEX

Endesa Chile IR presentation YE 2012

33

“This document is the property of ENDESA and therefore must not be disseminated or published without ENDESA's prior written consent.

The content of this document is provided for information purposes only and therefore has no contractual substance and should not be used as part of or construed as a legal contract.

ENDESA does not assume any responsibility for the information contained in this document and does not offer any implicit or explicit guarantees of the impartiality, accuracy and completeness of

this information and the opinions and statements contained therein. It shall also not be liable for any loss or damages that could arise as a result of using this information.

ENDESA does not guarantee that the forward-looking statements in this document will apply in the future in the terms set forth. Neither ENDESA nor its subsidiaries intend to update suchestimates, forecasts and objectives contained herein, except where required to do so by law”.